Closing Corporate Loophole Would Make MD’s Taxes More Fair and Generate Needed Revenue

By closing a loophole in the way corporations report their earnings, Maryland can make its tax system fairer and generate needed revenue for schools, public safety and other services.

The Senate Budget and Taxation Committee will take up legislation today that would close the door to a range of currently legal accounting tactics businesses use to avoid paying taxes to the state. The Maryland Center on Economic Policy will join others in testifying in support of the Business Relief and Tax Fairness Act (HB 1298/SB 395).

The legislation would treat a parent company and its subsidiaries as one corporation for state income tax purposes, a concept known as ‘‘combined reporting.’’

Combined reporting provides a more complete and accurate accounting of the profits corporations earn from their activities in Maryland. For example, under current law, a company can establish a subsidiary in a state with a lower tax rate and shift its earnings there on paper by purchasing goods from the subsidiary at artificially high prices. The legislation would end this tax avoidance tactic.

Combined reporting also helps put smaller, locally-owned corporations with no presence outside of Maryland on a more equal tax footing with larger companies that operate in many states. This level playing field helps protect local jobs.

By stemming the flow of profits earned here to other states, combined reporting will also have the benefit of raising revenue for education and other public services that bolster Maryland families, businesses and our economy. The Department of Legislative Services estimatesthat Maryland would collect tens of millions of dollars in additional revenue annually.

Maryland faces serious and well-documented needs in education, healthcare, public safety , environmental quality, and many other areas. But the state doesn’t have adequate resources to meet those needs, threatening further damaging cuts . The additional revenue from combined reporting is crucial to preventing those cuts.

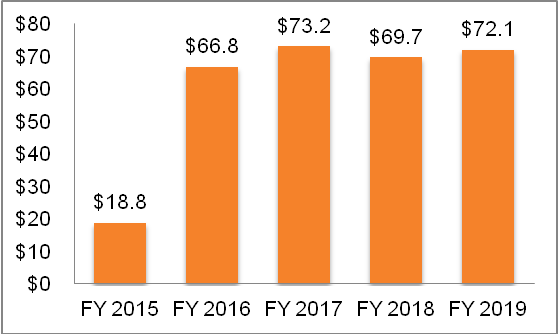

Combined Reporting WOULD BRING NEEDED REVENUE TO MARYLAND

Source: Maryland Department of Legislative Services

(Click to enlarge)

Combined reporting is well-established around the country. Twenty-three of the 45 states with corporate income and similar business taxes and the District of Columbia use combined reporting. Because it is so common, most large corporations that would be subject to a Maryland combined reporting law already have experience using it elsewhere. Maryland will not be breaking any new ground with this proposal.

|

States with Combined Reporting

|

||

|

Alaska

|

Kansas

|

New Mexico

|

|

Arizona

|

Maine

|

New York

|

|

California

|

Massachusetts

|

North Dakota

|

|

Colorado

|

Michigan

|

Ohio

|

|

District of Columbia

|

Minnesota

|

Utah

|

|

Hawaii

|

Montana

|

Vermont

|

|

Idaho

|

Nebraska

|

West Virginia

|

|

Illinois

|

New Hampshire

|

Wisconsin

|

Though corporate accounting practices may seem obscure, they have major implications for whether Maryland is able to collect enough revenue to fund the public services and investments that support Maryland residents and business. By implementing combined reporting, Maryland would create a more fair, effective, and productive corporate tax system.