DLS Report Shows Trade-offs from Reducing Corporate Income Tax Bring More Harm than Good (Updated)

The costs of reducing Maryland’s corporate income tax rate outweigh any potential benefits, according to a recent report from the state’s Department of Legislative Services. Reducing the rate has receivedrenewed attentionin recent months, but this report should serve as a warning to policymakers of all stripes.

The corporate income tax is an important source of income for the state. In fiscal year 2012, Maryland raised $877.9 million through the corporate income tax. This represented 5 percent of general fund revenue. These funds pay for many important programs and services—such as education, transportation, and health care—that benefit Marylanders and businesses alike.

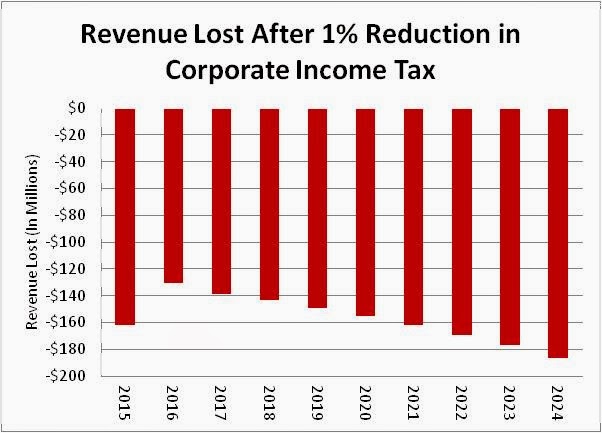

The DLS report projected the revenue that would be lost each year if Maryland were to reduce its corporate income tax rate by 1 percent, from the current rate of 8.25 percent to 7.25 percent:

(Click to enlarge all figues)

The DLS projects that the total cost of a 1 percent corporate tax reduction over ten years is just short of $1.4 billion.

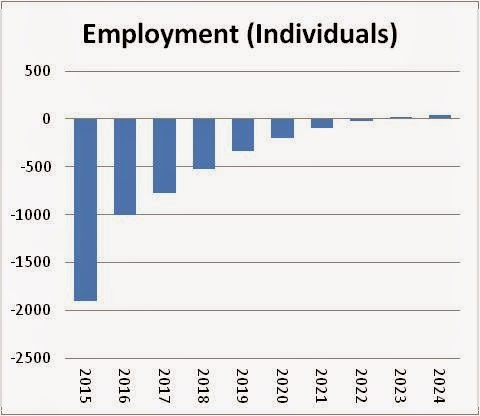

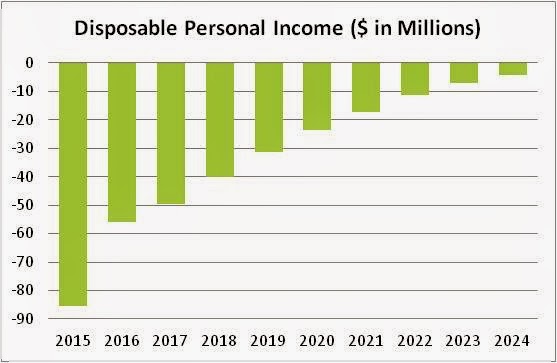

In light of recent projections indicating that Maryland will face a structural budget deficit in the upcoming year and the constitutional requirement to pass a balanced state budget, any loss of revenue from the corporate income tax must be offset by some mix of spending reductions or additional revenues from other sources. The DLS report models two different scenarios: one in which a loss of revenue is offset solely through reduced government spending, and another in which lost revenue is offset through an increase in sales taxes. The DLS projects consider the impact of these scenarios on employment in the state, disposable income available to residents, and economic migration in and out of Maryland.

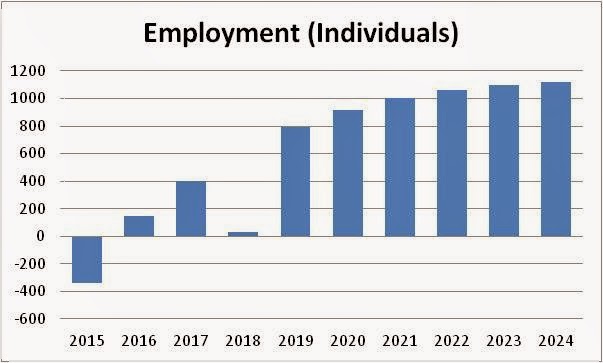

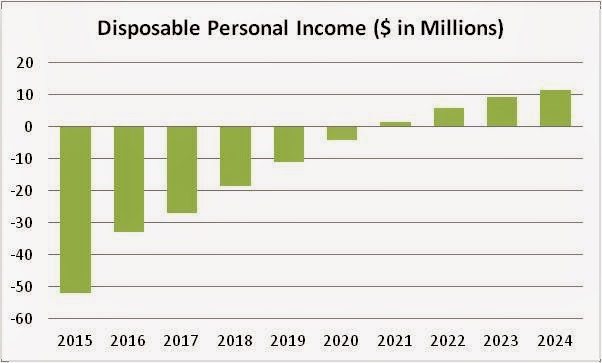

Scenario 1: Reduce Government Spending to Match Reduced Revenues

The DLS report rightly notes that reductions in government spending come at a cost. Because government spending is relatively labor intensive, budget cutbacks tend to reduce government employment, which in turn leads to private sector job losses as a result of lower overall demand in the economy. As a result, accounting for reduced corporate income tax collections solely through reductions in government spending results in net job losses for the foreseeable future and reduced disposable income for Maryland residents:

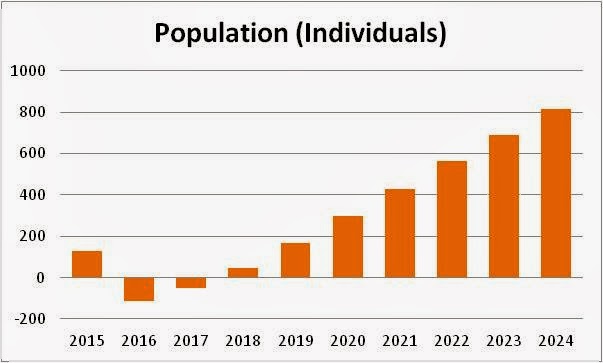

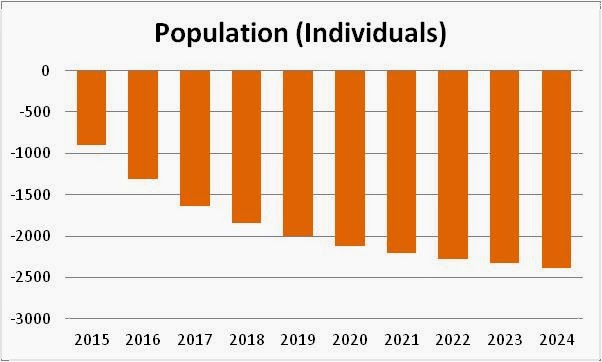

Scenario 2: Increase in State Sales Tax to Replace Foregone Revenues

In the second scenario, the decrease in the corporate income tax is offset by increases in the state sales tax. Increasing the state’s sales tax effectively raises consumer prices. While the DLS models indicate that this option has a less negative effect on employment and personal income than the previous scenario, they also find that it will result in increased economic migration as residents leave due to higher prices for goods subject to the sales tax:

It should also be noted that shifting more of the burden of state taxation to the sales tax would increase the inequality of Maryland’s tax system, especially when paired with a reduction in the corporate tax rate. Sales taxes, because they do not account for income, fall hardest on those least able to pay. Pairing such a shift with a massive giveaway to business would merely amplify the disparity between Maryland’s most and least fortunate.

Neither scenario indicates that reducing the corporate income tax would be a good idea for Maryland at this time. No matter what mix of spending reductions and tax increases policymakers choose to employ to offset lost revenue, reducing the corporate income tax shifts the cost to low and moderate income families who will see a reduction of jobs and public services as well as an increased tax burden. So why would anyone think this is a good idea?

Update (11.13.13):

Survey results released by Gonzales Research and Marketing Strategies find that 57% of Maryland residents oppose reducing the corporate income tax. (h/t Maryland Reporter)